Nifty Price Action Investopedia

Short Straddle Options Strategy : Detailed Research Report

Short straddle options strategy - where an investor sells both a call & a put option on the same underlying asset, with the same strike price and expiration date. The goal is to profit from the premiums received from selling both options, as they will expire worthless if the price remains stable.

OPTION STRATEGY

Doctor Amir & Shamala

Executive Summary:

The short straddle is a sophisticated options trading strategy primarily employed by experienced traders seeking to capitalise on periods of low market volatility. This strategy involves the simultaneous sale of both a call option and a put option on the same underlying asset, sharing an identical strike price and expiration date. While it offers the advantage of immediate income generation through premium collection and benefits from time decay, its risk-reward profile is characterized by a limited maximum profit and a theoretically unlimited maximum loss. The success of a short straddle hinges not only on the underlying asset remaining stable but also on a contraction in implied volatility, making it a nuanced approach requiring diligent monitoring and robust risk management.

1. Introduction to the Short Straddle Options Strategy

1.1 Definition and Core Principles

A short straddle is an advanced options strategy constructed by simultaneously selling (writing) a call option and a put option for the same underlying asset, both with the same strike price and the same expiration date. This configuration creates a market-neutral position, as the trader does not anticipate a significant directional movement in the underlying asset's price. Instead, the fundamental objective of the short straddle is to profit from a lack of volatility, specifically when the underlying asset is expected to remain relatively stable or trade within a narrow range until the options expire.

The term "neutral" in this context extends beyond merely expecting no price movement. The strategy explicitly benefits from a decrease in implied volatility over the life of the options contracts. This suggests that a trader might initiate a short straddle not just when predicting price stagnation, but more critically, when they believe implied volatility is currently inflated and is likely to contract. Therefore, the short straddle functions as much as a "short volatility" play as it does a "neutral" one, where the decline in the market's expectation of future price swings contributes significantly to profitability.

1.2 Construction: Selling Call and Put Options

To implement a short straddle, a trader executes two distinct yet simultaneous sell orders:

Selling a Call Option: This obligates the seller to deliver the underlying asset at the specified strike price if the option buyer chooses to exercise their right to purchase it.

Selling a Put Option: This obligates the seller to buy the underlying asset at the specified strike price if the option buyer chooses to exercise their right to sell it.

Both options are typically chosen to be "at-the-money" (ATM), meaning their strike price is very close to the current market price of the underlying asset. This selection is strategic, as ATM options generally possess the highest extrinsic value, thereby maximizing the premium collected by the seller. However, advanced traders may deviate from a perfectly ATM strike. For instance, if a subtle bullish bias is held, a trader might sell a straddle with a strike price slightly above the current underlying price. Conversely, for a bearish skew, the strike might be set slightly below the current price. This demonstrates that while the core concept is market neutrality, the "neutral" aspect can be fine-tuned. It is not always about anticipating absolute stagnation, but rather expecting the asset to remain within a specific, pre-defined range that can be strategically adjusted based on a more nuanced market perspective. This customisation adds a layer of complexity and potential for strategic adaptation beyond a purely non-directional approach.

1.3 Market Outlook and Ideal Conditions for Implementation

The short straddle is ideally suited for market environments characterised by low volatility and an expectation that the underlying asset's price will remain relatively stable or trade within a narrow range until the options expire.Traders frequently deploy this strategy when implied volatility (IV) is unusually high, as elevated IV inflates the premiums received from selling the options.This offers a larger potential profit should the options decay in value as anticipated. The ultimate objective is for both the sold call and put options to expire worthless, allowing the trader to retain the entirety of the collected premium.

The effectiveness of this strategy is deeply intertwined with the interplay of implied volatility and time decay. The strategy thrives when implied volatility is elevated at the point of entry, as this translates into higher premiums for the seller. Subsequently, the expectation is that this elevated implied volatility will decrease (a phenomenon known as volatility contraction) as time passes and the options approach expiration. This dynamic provides a dual benefit for the short straddle seller: initial high premium collection followed by the erosion of that premium due to both time decay and a reduction in market uncertainty. This highlights that the ideal scenario is not merely low realised volatility, but rather high implied volatility at entry that is then expected to decline, underscoring the critical role of volatility analysis as a primary driver for initiating this trade, rather than solely relying on a flat price forecast.

2. Profit and Loss Profile

2.1 Maximum Profit Potential: Premium Collection

The maximum profit achievable with a short straddle is precisely limited to the total premium collected from selling both the call and the put options.This optimal outcome materializes if the underlying asset's price at expiration is exactly at the common strike price. In this specific scenario, both the call and put options expire worthless, allowing the seller to retain the entire initial credit.

It is important to acknowledge that the probability of the underlying asset closing exactly at the strike price at expiration is exceedingly low. However, the strategy's profitability is not entirely contingent on this precise outcome. Partial profit can still be realised if the underlying price closes between the two breakeven points. This indicates that while the theoretical maximum profit is a specific point, the practical objective for traders is often to ensure the underlying asset remains within the broader profitable range defined by the breakeven points, leveraging the ongoing time decay within that zone. Consequently, traders should focus on the overall profit zone rather than fixating on the elusive exact strike price at expiration.

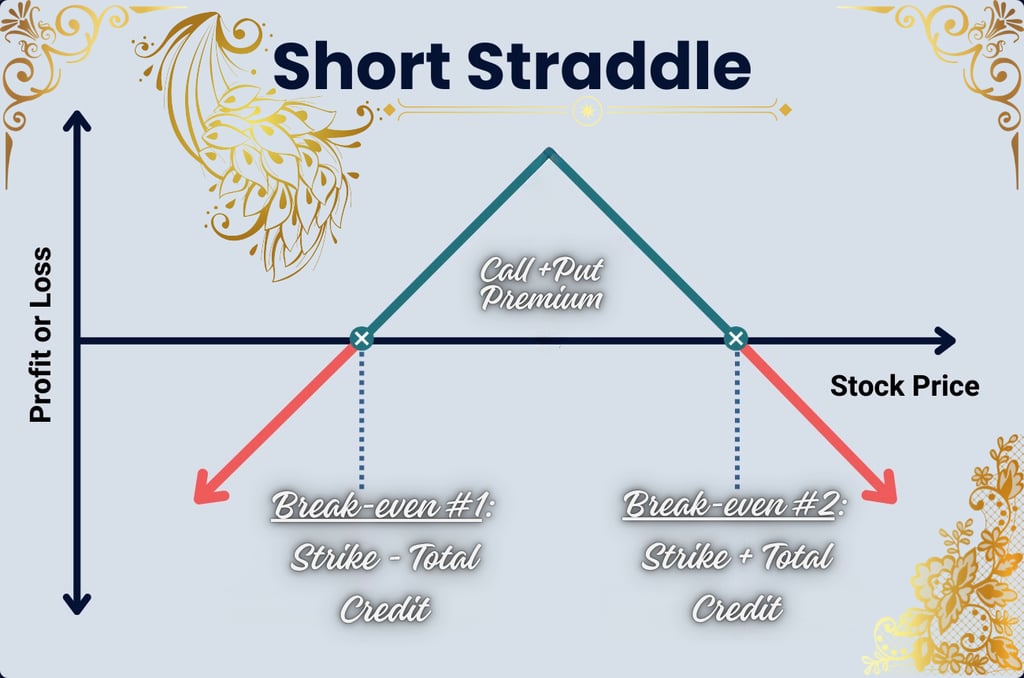

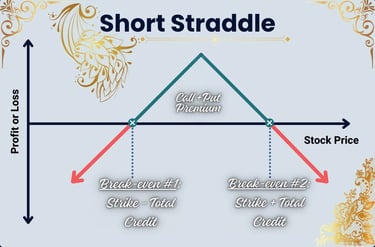

2.2 Breakeven Points Calculation

A short straddle is characterized by two breakeven points, which delineate the price range within which the strategy will generate a profit. These points are calculated by adding and subtracting the total premium received from the common strike price:

Upper Breakeven Point: Strike Price + Total Premium Received

Lower Breakeven Point: Strike Price – Total Premium Received

For example, if a straddle is sold at a $60 strike price for a total premium of $7.50, the upper breakeven point would be $67.50 ($60 + $7.50), and the lower breakeven point would be $52.50 ($60 - $7.50). The strategy yields a profit if the underlying asset's price at expiration remains strictly between these two calculated points.

These breakeven points are more than just static price levels; they function as dynamic volatility thresholds. A higher premium collected, often a direct consequence of higher implied volatility at the time of entry, effectively widens the profitable range. This means that the breakeven points directly reflect the market's expectation of future price movement and the compensation the seller receives for assuming the associated risk. A wider breakeven range provides a greater "cushion" against adverse price movements, but it can also signify that the market perceives a higher degree of risk, demanding a larger premium in return.

2.3 Maximum Loss Potential: The Unlimited Risk

The most critical characteristic and primary disadvantage of the short straddle is its theoretically unlimited maximum loss potential. This severe risk materializes if the underlying asset's price moves significantly away from the strike price in either direction, exceeding the calculated breakeven points.

Upside Risk: If the stock price experiences a sharp increase, the short call option becomes deeply in-the-money. The seller is then obligated to deliver shares at the lower strike price. If the trader does not already own the underlying shares, they would be forced to purchase them at the much higher current market price to fulfill this obligation, leading to substantial, uncapped losses.

Downside Risk: Conversely, if the stock price plummets, the short put option becomes deeply in-the-money. The seller is then obligated to buy shares at the strike price, which could be significantly higher than the asset's depreciated market value, resulting in considerable losses that can theoretically extend down to the underlying asset's price reaching zero.

This inherent unbounded risk profile necessitates extreme caution and the implementation of robust risk management techniques. The strategy is typically recommended only for experienced traders who possess a deep understanding of market dynamics and the discipline to manage such exposure. The inherent paradox of this strategy is that it is designed for a "neutral" market outlook, yet it carries "unlimited loss potential". This creates a fundamental tension: a strategy that bets on stability faces catastrophic risk from unexpected instability. The "neutral" outlook refers to the expected outcome under normal conditions, while the unlimited loss refers to the worst-case outcome resulting from an unforeseen, significant market move. This distinction underscores that "neutral" in options trading does not equate to "low risk." Instead, it implies a specific type of risk: the risk of an unexpected, large movement away from the central price expectation. This characteristic demands a strong conviction in low volatility and comprehensive contingency planning.

3. Advantages of the Short Straddle

3.1 Income Generation through Premium Collection

A primary appeal of the short straddle is its capacity for immediate income generation. By simultaneously selling both a call and a put option, the trader collects premiums from both sides of the trade, establishing a net credit position at the outset. This upfront cash flow is a significant draw for options traders focused on generating consistent income from their portfolios.

3.2 Profitability in Low Volatility Environments

The short straddle is specifically engineered to be profitable when the underlying asset's price remains stable or exhibits minimal movement within a tight range. This makes it an effective strategy for capitalizing on periods of market stagnation or when an anticipated event, such as an earnings report or a central bank announcement, does not result in the significant price swings that some other strategies depend upon. It offers a means for traders to profit even when they lack a strong directional conviction for the underlying asset.

3.3 Benefit from Time Decay (Theta)

Time decay, represented by the Greek letter Theta, is a substantial advantage for the seller of a short straddle. As time passes and the options approach their expiration date, their extrinsic value - the portion of their premium attributed to time and volatility - erodes. Since the short straddle involves selling options, this erosion of value directly benefits the trader, increasing the likelihood that both options will expire worthless and allowing the seller to retain the full premium collected. This decay effect accelerates significantly in the final weeks and days leading up to expiration, making shorter-dated options particularly attractive for this strategy. The accelerating power of Theta, especially as expiration approaches, means that small, consistent gains from time decay can accumulate. This suggests a strategic bias towards shorter-term expirations for short straddles, as the rapid decay provides a more potent profit driver, assuming the underlying remains stable. Consequently, monitoring the "time to expiration" becomes as critical as monitoring price movement.

4. Disadvantages and Key Risks

4.1 Unlimited Loss Exposure Explained

As previously detailed, the most severe risk inherent in a short straddle is its theoretically unlimited loss potential. This catastrophic outcome occurs if the underlying asset's price moves significantly beyond the breakeven points in either direction.

On the upside, if the stock price surges dramatically, the short call option becomes deeply in-the-money. The seller faces an obligation to deliver shares at the lower strike price. If they do not possess the underlying shares, they are compelled to purchase them at the much higher prevailing market price to fulfill this obligation, leading to substantial and uncapped financial losses. Conversely, on the downside, if the stock price plummets, the short put option becomes deeply in-the-money. The seller is then obligated to acquire shares at the strike price, which could be considerably higher than the asset's depreciated market value, resulting in significant losses that can extend to the underlying asset's price falling to zero. This unbounded risk profile mandates extreme caution and the implementation of robust risk management protocols.

4.2 Sensitivity to Market Volatility (Vega Risk)

The short straddle exhibits negative Vega, an option Greek that measures an option's sensitivity to changes in implied volatility. This means that the value of the short straddle decreases when implied volatility decreases, which is a favorable outcome for the trader. Conversely, an unexpected surge in implied volatility can rapidly transform a profitable position into a significant loss, even if the underlying asset's price remains within the initially anticipated range. This occurs because higher implied volatility inflates the value of both the sold call and put options, thereby increasing the cost required to close the position.

The relationship between volatility and the short straddle is a double-edged sword. While the strategy benefits from high implied volatility at entry because it allows for the collection of larger premiums, it simultaneously requires implied volatility to decrease over the course of the trade to realize maximum profitability. This creates a delicate balance. If volatility remains persistently high or increases unexpectedly after the trade is initiated, the initial advantage of collected premium can be quickly negated by the rising value of the outstanding options. This dynamic underscores the critical importance of sophisticated volatility analysis and the willingness to proactively exit the trade if volatility trends unfavorably.

4.3 Assignment Risk and Its Implications

As the seller of options, a short straddle trader assumes assignment risk. This means that if the underlying asset's price moves significantly in either direction, one or both options may become in-the-money and be exercised by the option buyer.

For the short call, if the underlying price rises above the strike price, the trader may be assigned and compelled to sell the underlying shares at the strike price. If the trader does not already own these shares, they must purchase them at the current (higher) market price to fulfill the obligation, incurring a loss. For the short put, if the price falls below the strike price, the trader may be assigned and forced to buy the underlying shares at the strike price, potentially at a price significantly higher than the current market value. While assignment most commonly occurs when an option is deep in-the-money near expiration, American-style options can be assigned at any time prior to their expiration date. This risk introduces an operational complexity and can lead to unexpected capital requirements or forced transactions.

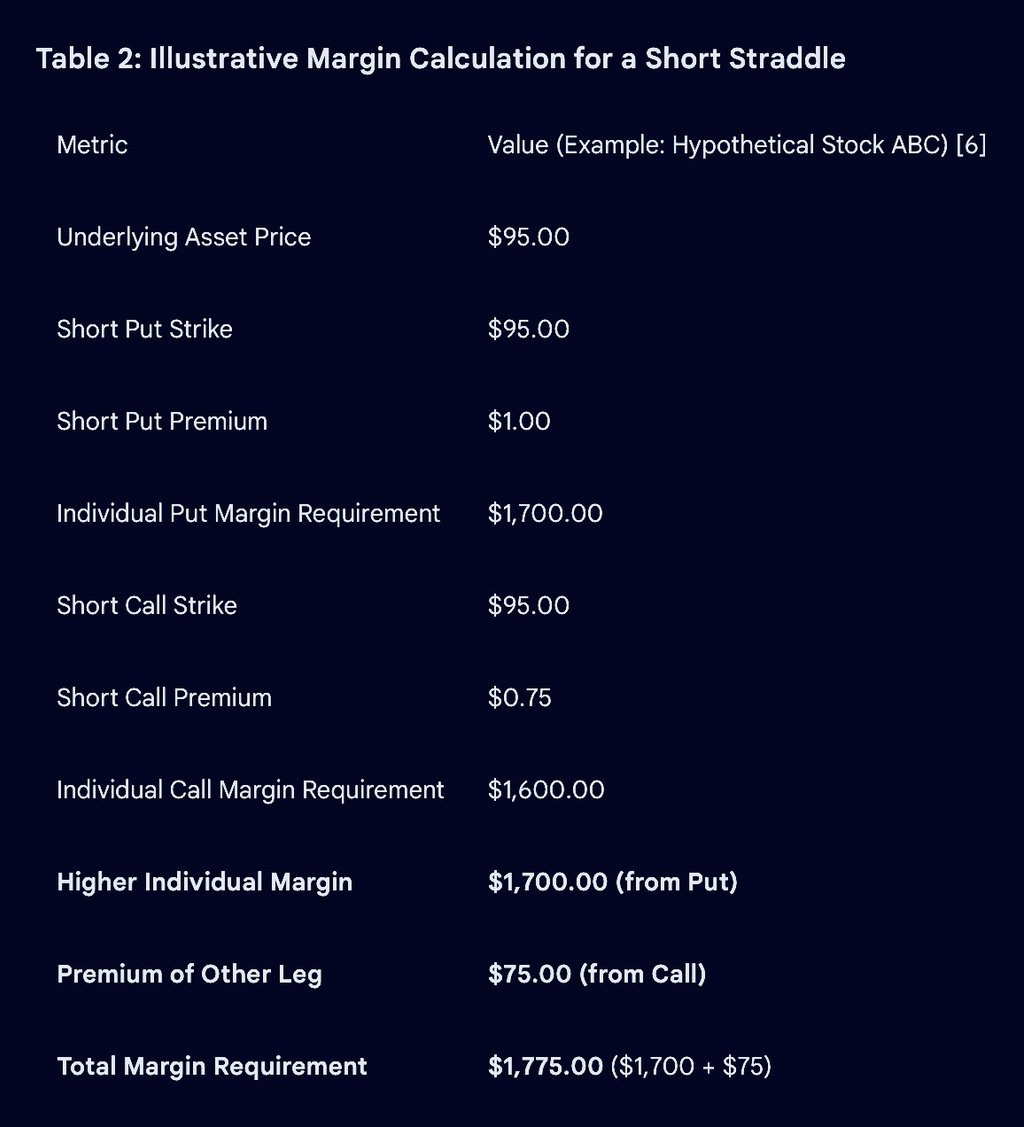

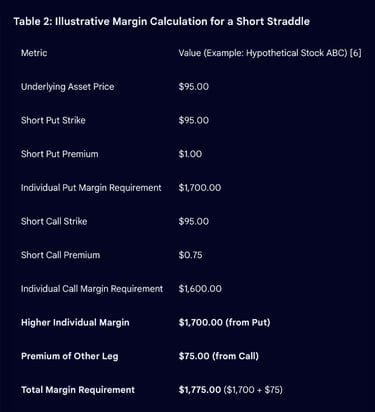

4.4 Margin Requirements

Due to their theoretically unlimited risk profile, short straddles necessitate substantial margin collateral. Brokerage firms require this capital to be held in the account as a safeguard against potential losses from adverse price movements. The margin requirement is typically calculated based on the higher of the two individual legs' (call or put) uncovered margin requirements, with the premium received from the other leg often added to this amount. This can result in a significant portion of a trader's capital being tied up, thereby impacting their overall buying power and limiting their ability to deploy capital in other opportunities.

The substantial margin requirements carry an inherent opportunity cost. The capital locked as margin could otherwise be earning interest in a risk-free asset or be deployed in alternative investments. This implies that traders must consider not only the absolute margin amount but also the potential returns forgone by having that capital immobilized. This factor renders the short straddle less capital-efficient compared to strategies with defined risk and lower margin demands, even if the potential premium collection appears attractive. The effective return on capital must therefore account for this implicit cost.

4.5 Gamma Risk and Delta Sensitivity Near Expiration

Gamma is an option Greek that measures the rate of change in an option's delta for a one-point movement in the underlying asset. For a short straddle, gamma is negative. This implies that as the underlying asset moves away from the strike price, the delta of the overall position will change more rapidly, accelerating the directional exposure and potential for loss.

Gamma risk is particularly pronounced as the options approach expiration, as gamma values tend to peak when the underlying price is near the strike. This phenomenon means that even small, seemingly insignificant price movements close to expiration can lead to a sudden and dramatic increase in the position's directional sensitivity and potential losses. It is akin to operating a vehicle where the steering becomes hyper-sensitive just before reaching the destination. This characteristic emphasizes why active management and potentially early closure are crucial for short straddles, especially as expiration nears. Holding a short straddle into expiration, particularly in a volatile market, is extremely risky due to gamma's amplifying effect on delta.

5. Impact of Option Greeks on Short Straddle Performance

The "Greeks" are a set of measures that quantify the sensitivity of an option's price to changes in underlying factors. Understanding their impact is fundamental to managing a short straddle.

5.1 Theta: The Time Decay Advantage

Theta quantifies the rate at which an option's extrinsic value erodes over time due to the passage of days. For sellers of options, as in a short straddle, theta is positive, meaning the strategy directly benefits from time decay. As each day passes, the extrinsic value of both the sold call and put options diminishes, contributing to the overall profit, provided the underlying price remains stable. This decay accelerates significantly in the final month or two before expiration, making shorter-dated options particularly attractive for this strategy due to the more rapid erosion of their time value.

5.2 Vega: Volatility's Influence

Vega measures an option's sensitivity to changes in implied volatility. A short straddle has a negative Vega. This characteristic means that if implied volatility decreases, the value of the sold options declines, which is beneficial for the trader. Conversely, an increase in implied volatility causes the value of the options to rise, leading to potential losses.Therefore, traders employing a short straddle ideally seek situations where implied volatility is high at the time of entry, allowing for greater premium collection, and is subsequently expected to decline over the life of the trade. This makes accurate volatility forecasting a critical component of successful short straddle deployment.

5.3 Gamma: Managing Delta's Rate of Change

Gamma measures the rate of change of an option's delta for a one-point movement in the underlying asset. For a short straddle, gamma is negative. This implies that as the underlying asset moves away from the strike price, the delta of the overall position will change more rapidly, increasing the directional exposure and potential for loss. Gamma risk is particularly acute as expiration approaches, as gamma values tend to peak, rendering the position highly sensitive to even small price fluctuations. This necessitates vigilant monitoring and proactive management, especially in the final stages of the trade.

5.4 Rho: Interest Rate Sensitivity

Rho measures an option's sensitivity to changes in the risk-free interest rate. Call options generally have positive Rho, meaning their value increases with rising interest rates, while put options have negative Rho, meaning their value decreases with rising interest rates. In a short straddle, which combines a short call and a short put at the same strike and expiration, the Rho effects tend to partially offset each other.

While Rho is generally considered the least impactful of the Greeks for short-term options, its significance increases for longer-dated options, such as LEAPS, and in market environments where interest rates are changing rapidly.For a short straddle, the net Rho exposure will depend on the relative Rho values of the individual call and put components, which can be influenced by their moneyness and time to expiration. The opposing Rho values of the short call and short put often largely cancel each other out, resulting in a generally minimal net impact on the straddle's overall value. However, for strategies involving longer expirations or a slight skew in the strike price selection, interest rate changes could introduce a subtle bias, potentially impacting overall profitability. This reinforces the principle that all Greeks, even those seemingly minor, contribute to the comprehensive risk profile of an options position.

6. Real-World Examples and Case Studies

6.1 Profitable Scenario Illustration

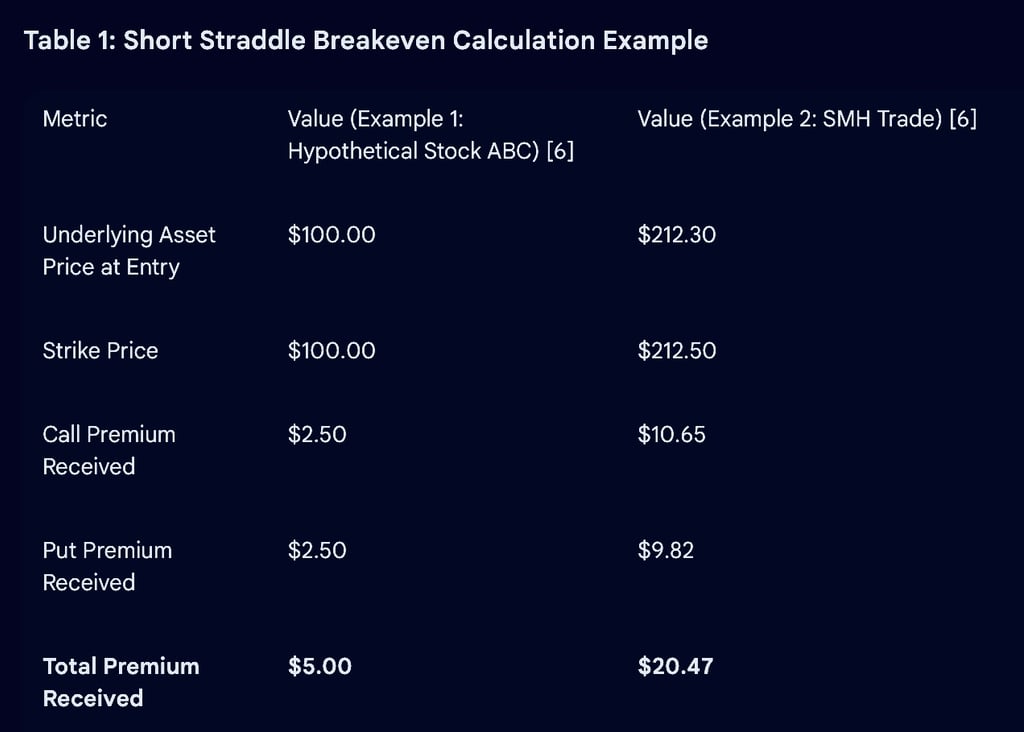

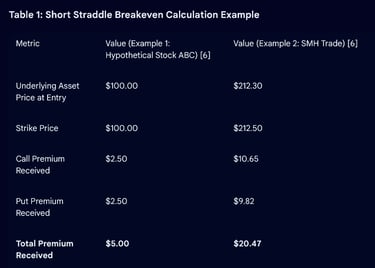

Example 1: Hypothetical Stock ABC Consider a scenario where a trader anticipates minimal movement in Stock ABC, currently trading at $100. The trader initiates a short straddle by selling a 100-strike call option for $2.50 and a 100-strike put option for $2.50, collecting a total premium of $5.00 per share (or $500 per contract).

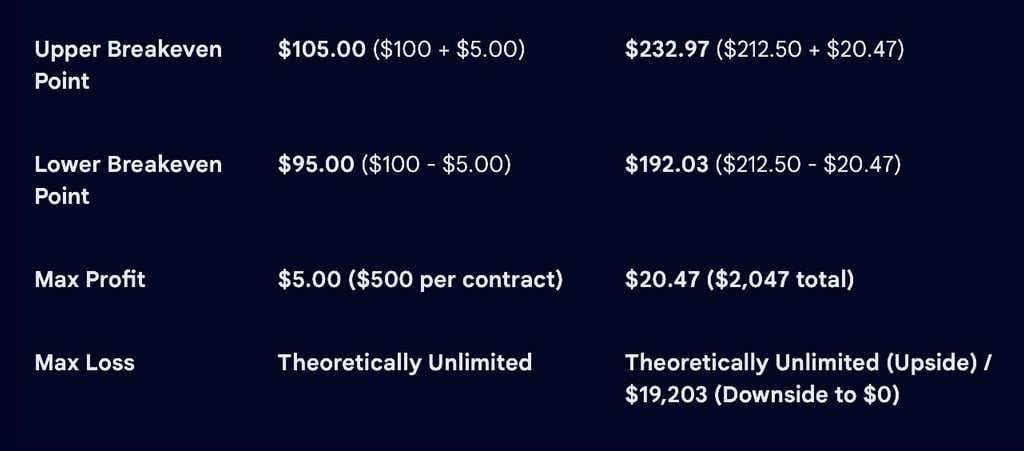

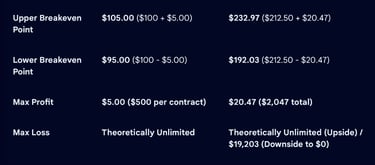

Breakeven Points: The upper breakeven point is $105.00 ($100 + $5.00), and the lower breakeven point is $95.00 ($100 - $5.00).

Outcome: If Stock ABC closes exactly at $100.00 at expiration, both options expire worthless, and the trader retains the full $500 profit. Even if ABC closes at $102.00, the call option is $2.00 in-the-money, but the $5.00 premium collected more than covers this, resulting in a partial profit. Similarly, if ABC closes at $97.00, the put option is $3.00 in-the-money, but the $5.00 premium still ensures a partial profit.

Example 2: SMH Trade Example (Semiconductor ETF) A more detailed example involves the SMH (Semiconductor ETF), trading at $212.30 with 35 days to expiration. A trader sells a 212.5 Call option for $10.65 and a 212.5 Put option for $9.82, resulting in a net credit of $20.47 per share (or $2,047 total for one contract).

Breakeven Prices: The upper breakeven is $232.97 ($212.50 + $20.47), and the lower breakeven is $192.03 ($212.50 - $20.47).

Outcome: If SMH moves from $212.30 to $212.00 at expiration, the call option expires worthless ($0.00). The put option expires $0.50 in-the-money, resulting in a $0.50 loss on that leg. The net profit is calculated as the total premium received minus the put loss: $20.47 - $0.50 = $19.97 per share, yielding a total profit of $1,997, which represents 97.6% of the maximum potential profit.

6.2 Unsuccessful Scenario Analysis

Example 1: Hypothetical Stock ABC (Significant Move) Using the same setup as the first profitable example (100-strike straddle, $5.00 premium, breakevens $95.00/$105.00):

Outcome 1 (Upside Loss): If Stock ABC rallies to $120.00 at expiration, the short call option is $20.00 in-the-money. The loss on this leg is $20.00 (in-the-money value) minus the $5.00 total credit received, resulting in a net loss of $15.00 per share, or $1,500 per contract. The put option would expire worthless.

Outcome 2 (Downside Loss): If Stock ABC collapses to $80.00 at expiration, the short put option is $20.00 in-the-money. The loss on this leg is $20.00 (in-the-money value) minus the $5.00 total credit received, resulting in a net loss of $15.00 per share, or $1,500 per contract. The call option would expire worthless.

Example 2: SMH Trade Example (Significant Downside Move) Using the same SMH setup (212.5-strike straddle, $20.47 premium, breakevens $192.03 / $232.97):

Outcome: If SMH moves from $212.30 to $180.00 at expiration, the call option expires worthless ($0.00). However, the put option expires $32.50 in-the-money, resulting in a $32.50 loss on that leg. The net profit/loss is calculated as the total premium received minus the put loss: $20.47 - $32.50 = -$12.03 per share, leading to a total loss of -$1,203.

These examples illustrate the inherent asymmetry of success and failure in a short straddle. While profits are capped at the premium collected, losses can be significantly larger, potentially extending to theoretically unlimited levels. This disproportionate risk-reward profile means that even a few losing trades can easily negate the gains accumulated from numerous successful ones. This characteristic underscores the critical importance of disciplined position sizing and strict risk management protocols for any trader employing this strategy.

7. Management and Adjustment Strategies

Effective management is paramount for mitigating the substantial risks associated with a short straddle, particularly given its unlimited loss potential. Proactive strategies are essential to navigate changing market conditions.

7.1 Early Position Closure for Profit or Loss Mitigation

Traders frequently opt to close a short straddle position prior to its expiration date, rather than holding it until the very end. This approach allows for locking in profits once a significant portion of the collected premium has decayed, typically aiming for a target profit percentage (e.g., 50% of the maximum potential profit). Conversely, early closure is crucial for limiting losses if the underlying asset's price begins to move unfavorably towards or beyond the established breakeven points. Implementing a predefined maximum loss threshold can guide this decision, ensuring that capital is preserved.

7.2 Rolling the Straddle: Adjusting Strike or Expiration

If the market outlook shifts or the position moves adversely, traders can "roll" the straddle. This involves closing the existing straddle and simultaneously opening a new one, often with a different strike price, a later expiration date, or a combination of both.

Rolling Out: Extending the expiration date provides the underlying asset more time to return to the profitable range or allows for further time decay to work in the trader's favour.

Rolling Up/Down: Adjusting the strike price can be employed if a directional bias begins to develop. For instance, if the stock starts trending upwards, the trader might roll the straddle up to a higher strike price, effectively converting it into a more directional neutral strategy or a short strangle, to better align with the new market sentiment.

7.3 Implementing Stop-Loss Orders

Given the theoretically unlimited loss potential of a short straddle, implementing stop-loss orders is a critical risk management technique. A stop-loss order automatically triggers the closure of the position if the underlying asset's price moves beyond a predetermined, acceptable loss level. This mechanism is particularly vital for managing unexpected spikes in volatility or rapid, adverse price movements, providing a crucial safeguard against catastrophic losses.

7.4 Continuous Monitoring of Market Volatility and Underlying Price

Effective management of a short straddle demands vigilant and continuous monitoring of both the underlying asset's price and market volatility (specifically, implied volatility). Traders must remain informed about upcoming economic news, earnings announcements, or any other significant events that possess the potential to trigger substantial price swings. Adjustments or early exits should be actively considered if market conditions deviate from the initial expectation of low volatility. The emphasis on "monitoring volatility" suggests a proactive rather than reactive approach to risk management. For a strategy with unlimited risk, merely reacting to significant market changes might prove too late. A proactive stance involves anticipating potential shifts and pre-emptively adjusting or exiting the position. This entails having a predefined exit plan for both profit realization and loss limitation, coupled with the discipline to execute that plan without hesitation, rather than hoping for a market reversal.

8. Comparative Analysis: Short Straddle vs. Other Strategies

Understanding the short straddle is enhanced by comparing it with other common options strategies, particularly those that also deal with volatility.

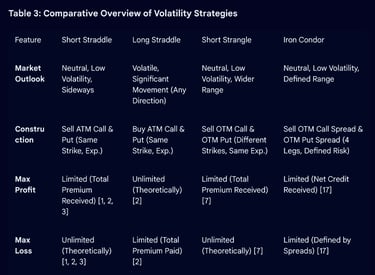

8.1 Short Straddle vs. Long Straddle

The short straddle and long straddle are diametrically opposed in their market outlook and risk-reward profiles:

Short Straddle: Involves selling both a call and a put option at the same strike and expiration date. It profits from low volatility and minimal price movement in the underlying asset. The maximum profit is limited to the premiums collected, while the maximum loss is theoretically unlimited.

Long Straddle: Involves buying both a call and a put option at the same strike and expiration date. It profits from high volatility and significant price movement in either direction (up or down). The maximum profit is theoretically unlimited, while the maximum loss is limited to the premium paid to establish the position.

The fundamental difference lies in their market outlooks: short straddles are a bet on stability, whereas long straddles are a bet on significant movement.

8.2 Short Straddle vs. Short Strangle

Both short straddles and short strangles are neutral, short-volatility strategies, but they differ in their construction:

Short Straddle: Involves selling a call and a put option at the same strike price (typically at-the-money) and the same expiration date. This results in a relatively narrower profitable range but generally higher premiums collected.

Short Strangle: Involves selling an out-of-the-money (OTM) call option and an OTM put option with the same expiration date, but different strike prices (the call strike is above the current price, and the put strike is below the current price). This creates a wider profitable range compared to a straddle, but typically yields lower premiums collected.

Both strategies carry theoretically unlimited risk if the underlying asset moves significantly beyond their respective breakeven points. The key distinction lies in the strike price selection, which dictates the width of the profitable range and the amount of premium collected, allowing traders to choose based on their specific risk tolerance and expectation for price movement within a defined range.

8.3 Short Straddle vs. Iron Condor

The short straddle and the iron condor represent different approaches to profiting from low volatility, primarily distinguished by their risk profiles:

Short Straddle: As discussed, this strategy has a theoretically unlimited loss potential and a limited maximum profit (equal to the premiums collected). It is a simpler two-leg structure that benefits from low volatility.

Iron Condor: This is a more complex four-leg strategy. It involves simultaneously selling an out-of-the-money (OTM) call spread (selling a call and buying a higher strike call) and an OTM put spread (selling a put and buying a lower strike put). A key advantage of the iron condor is its defined and capped maximum profit (the net credit received) and maximum loss. It also profits from limited price movement within a defined range.

Key Differences:

Risk Profile: The most significant distinction is the risk profile. The iron condor offers defined risk, making it appealing to traders who cannot tolerate the unlimited loss potential of a short straddle.

Profit Potential: The short straddle typically offers potentially higher maximum profit (the full premium of two at-the-money options) compared to the limited profit of an iron condor (the net credit from four options).

Complexity: The iron condor is inherently more complex due to its four-leg structure and multiple strike prices.

Capital Efficiency: Iron condors are often considered more capital-efficient due to their defined risk, as they require less margin than strategies with unlimited risk. However, commission costs can be higher due to the increased number of contracts involved.

Suitability: Both are neutral strategies for low volatility environments, but iron condors are generally preferred when risk definition and capital preservation are paramount.

The choice between a short straddle and an iron condor involves a fundamental trade-off between risk definition and expected return. Iron condors cap risk by purchasing "wings" (further out-of-the-money options), but this protection comes at the cost of sacrificing potential profit. Evidence suggests that hedging, as implemented in iron condors, can sometimes lead to a negative expected value, with strategies like short strangles (which are structurally similar to straddles) often showing superior performance in backtests. This implies that defining risk, while providing psychological comfort and preventing catastrophic losses, might reduce the expected theoretical return compared to strategies that embrace unlimited risk. Therefore, the decision between these strategies is not solely about risk tolerance but also about a philosophical approach to trading, weighing the perceived safety of defined risk against the statistical edge that might be diminished by the cost of protection.

9. Conclusion and Strategic Considerations for Traders

The short straddle is a powerful and income-generating options strategy, ideally suited for experienced traders who possess a strong conviction in low volatility and anticipate sideways price action in an underlying asset. Its primary appeal lies in the immediate collection of upfront premiums and the consistent benefit derived from time decay (Theta) as options approach expiration.

However, the strategy is accompanied by significant inherent risks, most notably its theoretically unlimited loss potential. This substantial downside, coupled with considerable sensitivity to unexpected increases in implied volatility (Vega) and accelerating gamma risk as expiration nears, demands rigorous and continuous risk management. Successful implementation of a short straddle hinges on several critical factors: accurate initial market assessment, disciplined position sizing to manage capital exposure, proactive monitoring of both price and volatility, and a clearly defined exit strategy for both profit realization and loss mitigation.

While the short straddle offers a distinct advantage in calm, range-bound markets, traders must be acutely aware of the substantial risks involved. The inherent asymmetry, where potential profits are capped but losses can be catastrophic, necessitates a high degree of discipline to adjust or close positions swiftly if market conditions deviate from the initial expectation. For those seeking to profit from low volatility but with a preference for defined risk, alternative strategies such as the Iron Condor, while sacrificing some profit potential, offer a more controlled and capped risk profile.

Ultimately, the short straddle serves as a compelling illustration of the nuanced and complex world of options trading. It demonstrates that high reward often accompanies high risk, and true mastery of such strategies stems from a deep understanding of both the mechanical construction of the trade and the underlying market forces at play. Beyond technical comprehension, the success of a short straddle heavily relies on the trader's psychological discipline. The repeated emphasis on "experienced traders," "robust risk management," and "continuous monitoring" for a strategy with unlimited loss potential and rapid Greek-driven changes highlights that emotional responses, such as fear or greed, can be devastating. The ability to cut losses quickly, resist the temptation to hold for maximum profit, and adhere strictly to a predefined trading plan is as crucial for success as the initial market analysis. This strategy is not merely a technical exercise but a profound test of a trader's emotional fortitude and adherence to a disciplined methodology.

Introduction to the Short Straddle Options Strategy

2. Profit and Loss Profile

3. Advantages of the Short Straddle

Table of contents

Daily analysis of Nifty price action trends.

Nifty price action - future trend prediction

© 2025 Nifty Price Action Invetopedia. All rights reserved.

Nifty price action investopedia

TO FOLLOW...

JOIN OUR SOCIAL MEDIA